Based on final Census Bureau data, the American Iron and Steel Institute (AISI) reported that the U.S. imported a total of 1,639,000 net tons (NT) of steel in November 2025, including 1,085,000 net tons (NT) of finished steel (down 5.2 percent and 18.7 percent, respectively, vs. October 2025). Total and finished steel imports are down 11.5 percent and 15.4 percent, respectively, year-to-date vs. 2024. Over the 12 month period December 2024 to November 2025, total and finished steel imports are down 10.5 percent and 13.3 percent, respectively, vs. the prior 12-month period. Finished steel import market share was an estimated 14 percent in November and is estimated at 19 percent over the first 11 months of 2025.

Key steel products with a significant import increase in November compared to October are heavy structural shapes (up 44 percent), blooms, billets and slabs (up 40 percent), line pipe (up 32 percent) and tin plate (up 18 percent). Products with a significant increase in imports over the 12-month period December 2024 to November 2025 compared to the previous 12-month period include tin plate (up 37 percent), line pipe (up 17 percent), wire rods (up 16 percent) and oil country goods (up 15 percent).

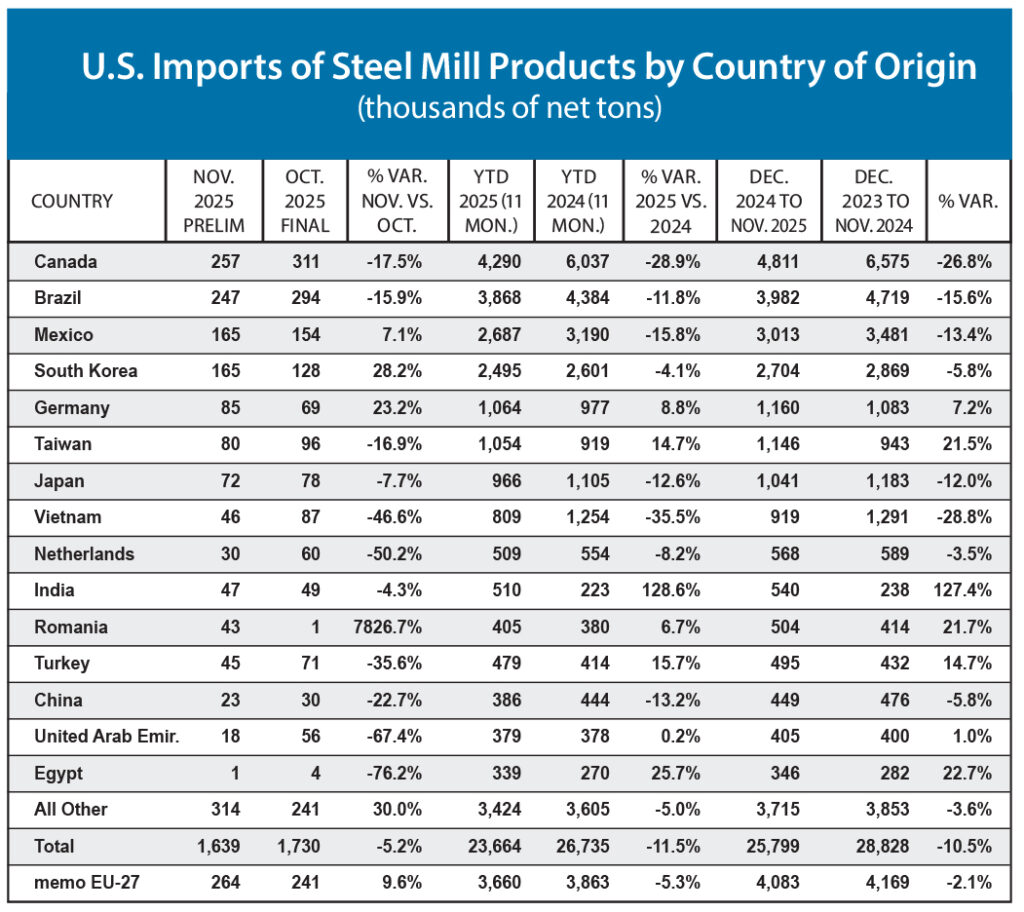

In November, the largest suppliers were Canada (257,000 NT, down 18 percent vs. October), Brazil (247,000 NT, down 16 percent), Mexico (165,000 NT, up 7 percent), South Korea (165,000 NT, up 28 percent) and Germany (85,000 NT, up 23 percent). Over the 12-month period December 2024 to November 2025, the largest suppliers were Canada (4,811,000 NT, down 27 percent vs, compared to the previous 12-months), Brazil (3,982,000 NT, down 16 percent), Mexico (3,013,000 NT, down 13 percent), South Korea (2,704,000 NT, down 6 percent) and Germany (1,160,000 NT, up 7 percent).

The largest suppliers were Canada (257,000 NT, down 18 percent vs. October), Brazil (247,000 NT, down 16 percent), Mexico (165,000 NT, up 7 percent), South Korea (165,000 NT, up 28 percent) and Germany (85,000 NT, up 23 percent). Over the 12-month period December 2024 to November 2025, the largest suppliers were Canada (4,811,000 NT, down 27 percent vs, compared to the previous 12-months), Brazil (3,982,000 NT, down 16 percent), Mexico (3,013,000 NT, down 13 percent), South Korea (2,704,000 NT, down 6 percent) and Germany (1,160,000 NT, up 7 percent).

Published March 2026