by MAURA KELLER

According to an ongoing report by Transparency Market Research, by 2025 it is projected that there will be up to 2.2 billion tons of solid waste generated globally by cities.

As Thomas Walker, assistant project manager at NYC-based construction and development services firm CNY Group pointed out, this number has almost doubled since 2012; and building materials account for half of solid waste generated. In addition, according to Allied Market Research, the global construction and demolition (C&D) waste recycling market is expected to reach $149 billion by 2027.

“It is safe to say that we should expect more C&D waste, and our facilities and processes need to be prepared,” Walker said. “However, the industry is starting to become more knowledgeable and adept in dealing with these problems. With more projects adopting LEED or similar standards, many construction professionals are being exposed to waste management standards, and in turn, we are playing a bigger role in the education of the tradespeople about these ideas.”

Walker said this trickle-down effect, ultimately will better prepare stakeholders across the development landscape, for any potential legislation and requirements in the future.

“As we continue to build on our commitments to going green, there is also the possibility for innovation in sorting and recycling technologies as attention is garnered for this issue,” Walker said.

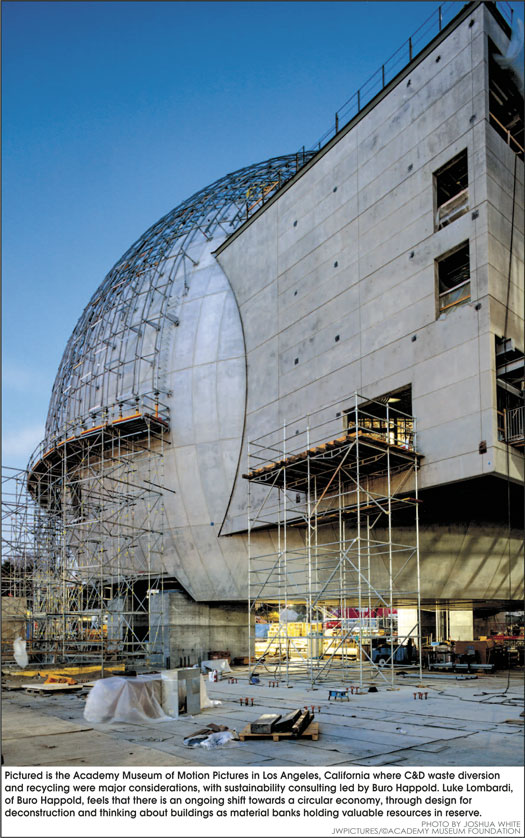

Luke Lombardi, P.E., senior sustainability engineer with Buro Happold’s Los Angeles office, said there is an ongoing shift towards creating and enabling a circular economy through design for deconstruction, use of material passports to track critical information, and thinking about buildings as material banks holding valuable resources in reserve.

“People at the forefront of this shift are exploring ways to leverage new technologies like blockchain, and major design firms are developing tools to support materials sharing and limiting waste during construction,” Lombardi said.

Isabelle Kavanagh, EIT, sustainability engineer with Buro Happold, pointed out that some building material manufacturers are creating takeback programs for their products (for example, Armstrong, USG, & CertainTeed ceilings, Mohawk, Interface and Starnet carpets, Tarkett flooring), that accept and recycle their products into new materials.

“It is important for industry professionals to be aware of these manufacturers and specify their products when possible, to encourage growth of a circular economy,” Kavanagh said. “There is also a trend towards innovation in the C&D waste industry, with some companies creating new products and materials from waste, such as Resin8 from CRDC, wood plastic composite from Conenor & Technalia, and Sika’s additive for concrete recycling. There is also innovation in the waste sorting and processing space, using robotics and other technology to automate processes.”

Growth Potential

William Turley, executive director of the Construction & Demolition Recycling Association (CDRA) said there are several key industry trends that C&D recyclers need to be aware of.

“There is increasingly limited landfill space and recycling markets are always challenging for construction materials. There is nowhere else to get rid of the material except to ship it by rail, barge or even truck across long distances out of state,” Turley said.

Turley also has seen an increase in regulation of waste, including C&D, by many states and localities that traditionally have not been as strict on oversight.

“This can be both good and bad. Overregulation can stifle markets, but there is a strong need to police bad actors,” Turley said. And many within the construction and demolition industry are seeing post-COVID growth as various sectors of the economy reopen, such as hospitality.

“Volume has increased across the board; which in turn causes more construction and demolition waste,” said Walker. “Construction professionals will have to determine how sites and projects can be built more efficiently in terms of providing input on material selection, reducing waste during construction, and having a plan for recycling inevitable waste.”

CNY Group has been working through this process on two multifamily housing development projects and found the most success through a combination of early discussions with all stakeholders, stringent QA/QC programs on site, and further innovation in technologies and processes.

“When we come to the table, we find that there is often the perception that these strategies are going to cost more, and while CNY Group has the data to show that’s not the case, it’s often a deterrent for some stakeholders,” Walker said. “In fact, between over-purchasing temporary or unnecessary materials and paying overtime for the labor to haul away waste at the end of the day, not recycling or having a plan to recycle is actually more costly in the long run.”

Legislative Initiatives in the C&D Recycling Space

Within the legislative and regulatory environment, it is mostly regulation that affects C&D recycling. As Turley explained, some states, such as California, are pushing hard to increase C&D recycling and improve markets. An example is the California Recycling Commission’s plan to increase the amount of recycled content to 10 percent from the current 4 percent for new drywall sold in the state.

Turley also pointed to Massachusetts Department of Environmental Protection (DEP), which has set a 15 percent minimum performance standard for C&D recycling facilities. If they don’t make that threshold, they are supposed to send all their material to a facility that does.

“Now, 15 percent may not seem high, but the DEP is including the denominator bulks, such as mattresses and furniture, which can be challenging to recover. The agency plans to increase that recycling rate in the future, even though as a consumer it doesn’t support construction material recycling markets,” Turley said.

Maine also is trying to legislate against the importation of out-of-state C&D material because facilities are taking in large amounts of it from throughout New England, recovering what they can and sending the residual to local landfills, which are being reduced in number.

“Disposal bans are also starting to pop up for some materials,” Turley said. “Massachusetts has been the most aggressive for many years, requiring that wood, concrete, asphalt, drywall and other materials pass through a recycling facility before it is disposed.”

Legislation with the most potential impact is environmental justice, which is also one of the two core focuses of the Biden Administration. Environmental justice legislation has already passed in New Jersey, and many other states are looking to copy those requirements.

“The tenets of this concept allow more community participation in allowing what businesses are allowed to operate in their area, especially in disadvantaged minority regions,” Turley said. “Facilities could be denied a permit to operate, or permit renewal, after years of operation, under these laws. The CDRA is helping its members manage these issues.”

In addition, some key legislation on the city and state level is largely focused on setting C&D diversion and recycling requirements. Some examples include:

•New York State Senate Bill S3148: The bill requires that contractors in New York State reuse or recycle at least 25 percent by weight of their C&D debris, for projects that have been issued a permit with an application date within one year of the effective date of the bill; and 50 percent by weight of C&D debris for projects issued a permit with an application of more than one year.

•New York State Senate Bill S6228 sets the same C&D recycling requirements for New York City specifically

•CalGreen C&D waste: CALGreen requires covered projects to recycle and/or salvage for reuse a minimum 65 percent of nonhazardous construction and demolition waste or meet a local construction and demolition waste management ordinance, whichever is more stringent.

Currently in NYC, which tends to lead the way in terms of sustainability policy, there is no required standard or benchmark for the recycling of C&D waste. As Walker explained, the Rules of the City of New York note that construction waste is and should be source separated and recycled – but there is a lack of legislation requiring recycling or certain minimum benchmarks.

“This is surprising given, per EPA statistics, the U.S. generated over 600 million tons of construction and demolition debris in 2018 – which doubles municipal waste in the same year,” Walker said. “Further, there are not many facilities that can handle the waste itself, which poses a significant challenge in terms of how much they can actually process. Considering these stats, it is inevitable that we can expect legislation soon to standardize and create requirements for waste diversion and recycling streams, and recycling of construction waste by tonnage.”

This is already the norm with LEED, which requires projects to recycle 50 percent of construction and demolition waste by ton at minimum, with at least three diversion streams. As Walker explained, the LEED points system has driven more awareness, and there are organizations that are helping to push the effort from a grassroots level.

“We feel strongly that these baseline requirements should be more widespread if we’re going to effectively combat the waste from the construction volume we’re seeing today,” Walker said.

Industry Challenges

One of the key challenges facing the C&D recycling industry is availability of C&D material recycling facilities in more remote areas of the country. As Kavanagh pointed out, in urban areas, there is often widespread and robust C&D waste collection, separation, transfer, and recycling facilities that enable C&D waste to be successfully recovered. The same cannot said for projects located in less urban areas – it’s still possible to sort and separate C&D waste on site, but there may not be an appropriate facility nearby that the materials can be taken to for processing.

“Also, recycling materials that are more difficult to recover, such as window glass, flooring, insulation, gypsum, composite materials and hazardous waste, remains a big challenge,” Kavanagh said. “The properties and makeup of these materials and/or the lack of effective technology for recycling them means that they are usually sent to landfill, decreasing diversion rates.”

Source separation can also be a challenge, especially when buildings are not designed for easy deconstruction. It requires extra effort, time, and physical space to separate out materials on project sites, causing challenges for the general contractor.

“If the source separation is not done carefully, it can also cause difficulties for the sorting and processing facilities and decrease the volume of material that can be properly recycled,” Kavanagh said.

“Government entities can do all the disposal bans they want, and because of extended producer responsibility (EPR), manufacturers want their products recovered, but at the end of the day if there is nowhere for the end product to go, it is going to a landfill,” Turley said. “Unfortunately there is often a lack of supportive regulation to allow recyclers to find those end markets.”

Another challenge is making sure the material is being recycled. Even if there is a requirement that a certain recycling rate be met by a facility, there is no guarantee that rate is being met outside of the word of the plant operator.

“This happens all the time in LEED, where untrue recycling rates are claimed for green building projects and points are awarded. The CDRA is working with USGBC to stop the cheating that has been going on for years under the recycling credits,” Turley said. “Another fundamental challenge is getting insurance for all waste facilities. There have been too many claims, especially around facility fires, and many carriers are no longer writing policies for the industry. Those that are still around have jacked up rates tremendously, making this an incredibly large part of the cost of doing business.”

Challenges aside, experts agree that the C&D recycling industry will continue to grow and demand for C&D recycling will increase. As such, C&D recyclers can work to expand their processing capacity, expand facility locations to areas with less available C&D recycling infrastructure, and look into innovative methods to recycle difficult to recover materials.

“We expect the recycling of construction materials to continue to grow for a variety of reasons. First is a push by states and municipalities that want to see more material recovered,” Turley said. “Second is the pressure EPR is putting on all manufacturers, including those for construction materials, which is spurring those manufacturers to strongly support environmentally friendly disposal options for their products, including closing the loop.”

Turley recommended C&D recyclers follow what is happening on the state and local regulation front. Related to that, also follow national recycling organizations. The CDRA is implementing a tool for members that will provide them with information on recycling and other important bills going through their state legislatures.

“These can impact your business more than most other factors,” Turley said.

Published in the April 2022 Edition